First Floor Incubator Building

Masdar City, Abu Dhabi, United Arab Emirates

Part 1 – Risk Management for Executive Leaders: Proactive Strategies for Resilience and Growth

In today’s dynamic economic landscape, effective risk management transcends merely avoiding losses; it is a strategic competency that balances risk with opportunity to achieve financial resilience and sustainable growth. Senior executives are tasked with navigating volatile markets, operational disruptions, and regulatory complexities, making robust risk management practices indispensable.

Risk Management Strategies equip executives with advanced tools and techniques to identify, assess, and mitigate financial risks, emphasizing the development of proactive and tailored risk management plans that align with organizational objectives. By embedding these strategies into their leadership practices, executives can safeguard organizational stability while capitalizing on emerging opportunities.

In an increasingly volatile and interconnected global economy, financial risks—spanning market fluctuations, credit defaults, regulatory changes, and operational inefficiencies—pose significant challenges to organizational success. For senior executives, effective risk management is not just a protective measure; it is a strategic tool that drives resilience, innovation, and sustainable growth.

Why Risk Management Matters?

In an increasingly uncertain business environment, risk management is not just a defensive strategy—it is a fundamental driver of long-term success. Organizations that proactively manage risks are better equipped to maintain financial stability, adapt to market disruptions, and seize growth opportunities. Whether safeguarding liquidity, protecting profitability, or enhancing stakeholder confidence, effective risk management empowers executives to make informed decisions that ensure resilience and sustainable development. The following key areas illustrate why risk management is essential for financial and strategic leadership.

- Safeguard Liquidity:

Cash flow is the lifeblood of any organization. Effective risk management ensures that an organization maintains adequate liquidity to fund operations, even during disruptions such as supply chain breakdowns or market downturns. By actively monitoring liquidity risks, executives can implement proactive measures like optimizing working capital or securing credit lines to maintain financial stability. - Protect Profitability:

Market volatility, rising costs, and economic downturns can erode profit margins. Risk management strategies such as hedging against currency or commodity price fluctuations enable leaders to stabilize costs and revenues, minimizing the financial impact of adverse conditions and ensuring consistent profitability. - Drive Strategic Decisions:

Risk management is not just about minimizing threats; it is also about enabling growth. By balancing risk and opportunity, executives can pursue initiatives that align with long-term strategic goals, such as entering new markets, launching innovative products, or investing in sustainability. For example, scenario planning helps leaders make informed decisions about resource allocation in uncertain environments. - Enhance Stakeholder Confidence:

Demonstrating robust risk management practices reassures investors, partners, and customers that the organization is resilient and well-prepared to navigate challenges. Transparency in risk identification and mitigation fosters trust, strengthening relationships and boosting the organization’s reputation in competitive markets.

The Broader Impact

Risk management is more than just a safeguard against financial and operational threats—it is a strategic enabler that allows executives to shift from reactive problem-solving to proactive leadership. By embedding risk management into their decision-making frameworks, senior leaders can anticipate challenges, mitigate disruptions before they escalate, and turn uncertainty into a competitive advantage./br>

A well-structured risk management approach fosters resilience at every level of the organization, ensuring stability during economic downturns, supply chain disruptions, and regulatory shifts. This resilience not only protects the core business but also creates an environment where calculated risks can drive innovation and expansion. Companies that integrate risk management into their strategic planning can confidently pursue growth opportunities, such as market entry, mergers, acquisitions, and digital transformation, while maintaining financial and operational security./br>

Furthermore, robust risk management enhances transparency and governance, strengthening trust with investors, partners, and stakeholders. Organizations that demonstrate foresight and preparedness are better positioned to attract funding, secure long-term partnerships, and maintain a strong reputation in competitive markets. Ultimately, a proactive risk management culture empowers organizations to navigate volatility with agility, ensuring they are not just surviving, but thriving in an ever-evolving economic landscape.

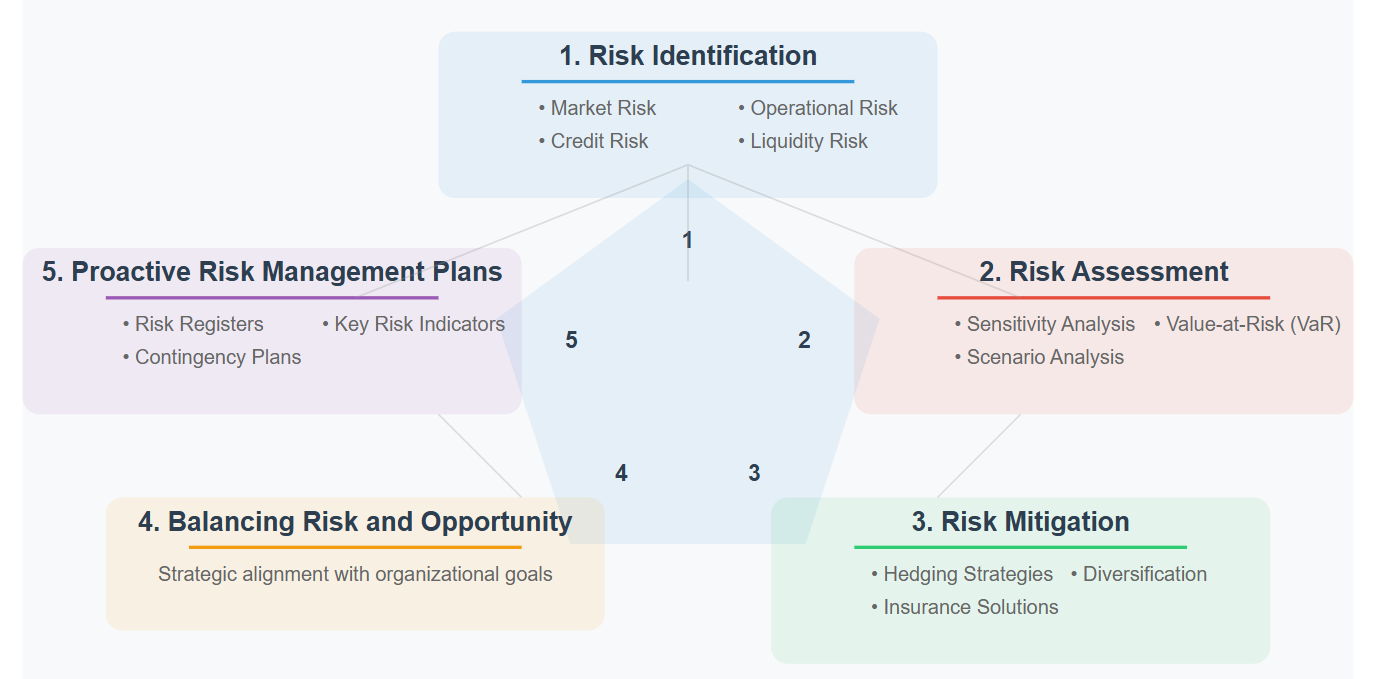

Core Components of Risk Management

In an unpredictable business landscape, a well-defined risk management framework is critical for maintaining stability and seizing growth opportunities. Rather than simply reacting to crises, forward-thinking executives integrate risk management into their strategic planning to enhance resilience, optimize decision-making, and sustain long-term success.

A robust risk management framework provides a structured approach to identifying, assessing, and mitigating risks, ensuring that potential threats are addressed before they escalate into significant disruptions. By systematically evaluating vulnerabilities and implementing proactive strategies, organizations can safeguard financial health, operational continuity, and stakeholder confidence. The following key components outline an effective risk management approach, equipping executives with the tools to navigate uncertainties while positioning their organizations for sustainable growth.

1. Risk Identification: Knowing What to Manage

Effective risk management begins with a thorough identification of vulnerabilities across the organization, categorized into distinct risk types:

- Market Risk: Fluctuations in interest rates, exchange rates, or commodity prices that can impact financial performance. For instance, a manufacturing company may face increased costs due to rising raw material prices.

- Credit Risk: Potential counterparty defaults or delays in customer payments, which can disrupt cash flow and financial stability.

- Operational Risk: Failures in internal processes, cybersecurity breaches, or supply chain disruptions. For example, a logistics company experiencing downtime in key systems risks losing customer trust.

- Liquidity Risk: Challenges in meeting short-term financial obligations, such as payroll or supplier payments, due to insufficient cash reserves.

2. Risk Assessment: Measuring Impact and Likelihood

Once risks are identified, their potential impact and likelihood must be assessed using qualitative and quantitative techniques. This evaluation enables informed decision-making and effective prioritization.

- Sensitivity Analysis: Examines how changes in key variables, such as interest rates or commodity prices, affect financial outcomes. For example, a construction firm can assess how fluctuations in steel prices impact project profitability.

- Scenario Analysis: Models potential outcomes under various economic or operational conditions, such as market expansion or supply chain disruptions.

- Value-at-Risk (VaR): Quantifies the maximum potential financial loss within a specific confidence interval, offering a clear picture of risk exposure.

3. Risk Mitigation: Reducing Likelihood and Impact

Proactive risk mitigation strategies help reduce exposure and minimize the financial impact of identified risks. Key approaches include:

- Hedging Strategies: Employ financial instruments like forward contracts or swaps to manage market risks such as currency or interest rate fluctuations.

- Insurance Solutions: Protect against operational disruptions or liabilities by securing appropriate coverage, such as cyber liability insurance for digital operations.

- Diversification: Spread investments or revenue streams across different markets, products, or geographies to minimize dependency on a single source.

4. Balancing Risk and Opportunity

Risk management is not solely about avoidance—it’s also about identifying and leveraging opportunities that arise from calculated risks. This approach ensures that:

- Decisions align with organizational goals.

- Resources are allocated toward initiatives that drive growth and innovation.

- Leaders capitalize on market shifts and emerging trends.

5. Developing Proactive Risk Management Plans

Tailored, forward-looking risk management plans provide a framework for navigating uncertainty. These plans typically include:

- Risk Registers: Comprehensive documentation of identified risks, mitigation strategies, and assigned accountability.

- Contingency Plans: Predefined responses to high-impact risks, ensuring continuity during unexpected disruptions.

- Key Risk Indicators (KRIs): Metrics that signal emerging risks and enable timely interventions.

Advanced Techniques for Financial Risk Management

In today’s dynamic financial landscape, advanced risk management techniques are essential for organizations seeking to maintain stability, optimize decision-making, and capitalize on emerging opportunities. By leveraging sophisticated tools and analytical methods, executives can not only mitigate risks but also enhance strategic resilience, enabling proactive responses to potential disruptions. The following key techniques are instrumental in modern financial risk management:

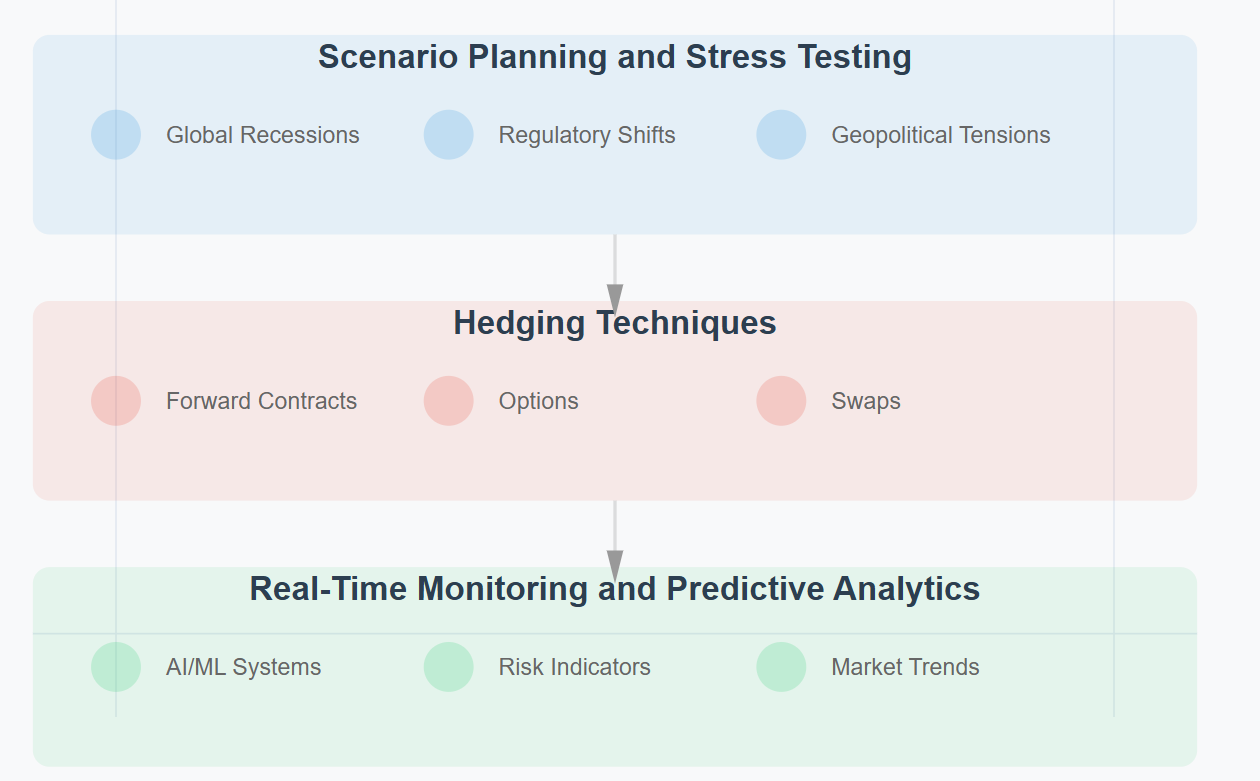

- Scenario Planning and Stress Testing:These methods allow organizations to model extreme economic conditions, such as global recessions, regulatory shifts, or geopolitical tensions, to assess their potential impact on financial stability. By simulating various risk scenarios, businesses can evaluate vulnerabilities and develop contingency plans, ensuring they remain agile and prepared for adverse market conditions. Leading institutions utilize stress testing to measure their resilience against economic shocks, liquidity crises, and fluctuations in consumer demand.

- Hedging Techniques:Hedging serves as a critical financial strategy to protect against unpredictable market fluctuations. Organizations exposed to currency, interest rate, or commodity price volatility can employ financial instruments such as forward contracts, options, and swaps to stabilize costs and revenues. For example, multinational corporations hedge against foreign exchange risk by locking in currency exchange rates, while commodity-dependent industries use futures contracts to manage raw material price fluctuations.

- Real-Time Monitoring and Predictive Analytics:In an era of rapid digital transformation, real-time monitoring systems powered by artificial intelligence (AI) and machine learning provide organizations with invaluable insights into emerging risks. By continuously analyzing key risk indicators, supply chain variables, and financial market trends, businesses can identify potential threats before they escalate. Predictive analytics further enhances risk management by forecasting potential disruptions, enabling companies to implement corrective actions in advance and optimize their operational strategies dynamically.

Conclusion

Effective risk management is an indispensable pillar of resilient and forward-thinking leadership. It equips executives with the tools to navigate uncertainties, safeguard organizational stability, and drive sustainable growth. By mastering techniques such as risk identification, scenario planning, sensitivity analysis, and hedging, leaders can proactively mitigate vulnerabilities while unlocking opportunities in volatile markets.

Part 2 of this blog will go in depth of challenges and solutions in risk management, best practices and real world applications of risk management in finance.

- Empowering Growth

- Driving Excellence

- Bridging Global Opportunities

Useful Pages

Where can You find us ?

Have any questions?

Phone: +971 56 603 1199

Need more information?

E-mail: info@nbglobalconsulting.com

2025, NB GLOBAL CONSULTING. All rights reserved. Made with ❤️ by ROSA eSolutions.